All Categories

Featured

Table of Contents

Which one you pick depends on your demands and whether or not the insurance company will certainly accept it. Policies can likewise last till defined ages, which for the most part are 65. Since of the countless terms it uses, level life insurance policy provides possible policyholders with versatile choices. Beyond this surface-level info, having a greater understanding of what these plans involve will certainly help guarantee you purchase a policy that satisfies your demands.

Be conscious that the term you select will certainly affect the premiums you spend for the plan. A 10-year degree term life insurance coverage plan will set you back much less than a 30-year policy due to the fact that there's much less chance of a case while the plan is energetic. Reduced threat for the insurance provider relates to lower premiums for the insurance holder.

Your family members's age need to likewise affect your plan term selection. If you have kids, a longer term makes sense since it protects them for a longer time. If your children are near their adult years and will be economically independent in the near future, a much shorter term could be a better fit for you than an extensive one.

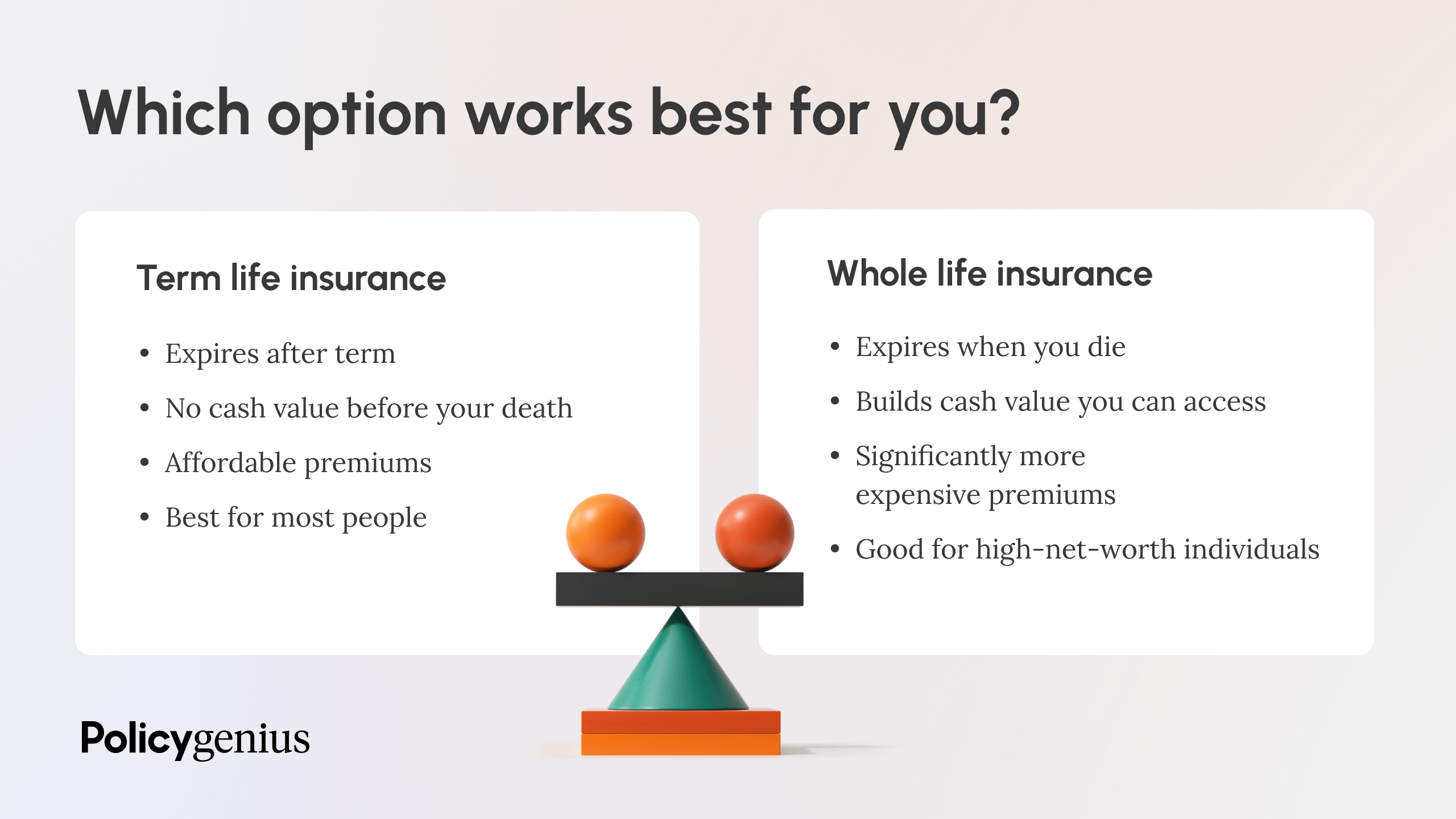

When comparing entire life insurance policy vs. term life insurance, it's worth keeping in mind that the last normally costs much less than the previous. The outcome is much more coverage with reduced costs, providing the very best of both worlds if you need a substantial quantity of protection yet can't afford a much more expensive plan.

What Makes Level Premium Term Life Insurance Policies Different?

A degree death benefit for a term policy normally pays out as a swelling amount. Some level term life insurance coverage business permit fixed-period settlements.

Passion settlements received from life insurance coverage plans are taken into consideration earnings and are subject to taxes. When your degree term life policy expires, a few different points can occur.

The drawback is that your eco-friendly degree term life insurance coverage will come with greater costs after its first expiry. Ads by Money.

Life insurance policy companies have a formula for calculating danger utilizing mortality and passion (term life insurance for seniors). Insurance firms have hundreds of customers securing term life plans simultaneously and utilize the premiums from its energetic policies to pay surviving beneficiaries of various other policies. These firms utilize mortality to estimate the amount of people within a particular group will file fatality insurance claims per year, which information is used to identify typical life span for potential insurance holders

Additionally, insurance coverage companies can invest the cash they receive from costs and boost their revenue. The insurance policy business can spend the cash and gain returns.

The following area information the benefits and drawbacks of level term life insurance. Foreseeable costs and life insurance protection Streamlined plan structure Possible for conversion to irreversible life insurance policy Minimal protection period No cash money value buildup Life insurance coverage costs can raise after the term You'll discover clear advantages when comparing degree term life insurance policy to other insurance kinds.

What is the Definition of Term Life Insurance With Accelerated Death Benefit?

From the minute you take out a policy, your costs will never change, helping you prepare economically. Your coverage will not vary either, making these policies effective for estate preparation.

If you go this path, your costs will certainly raise however it's always excellent to have some adaptability if you desire to maintain an energetic life insurance policy policy. Renewable level term life insurance policy is one more choice worth considering. These policies enable you to maintain your present strategy after expiration, giving adaptability in the future.

What is What Does Level Term Life Insurance Mean? Key Information for Policyholders

Unlike a whole life insurance policy policy, degree term insurance coverage doesn't last indefinitely. You'll select a coverage term with the very best level term life insurance policy prices, however you'll no more have insurance coverage once the strategy expires. This downside could leave you clambering to discover a brand-new life insurance policy plan in your later years, or paying a premium to prolong your existing one.

Numerous whole, global and variable life insurance policy plans have a money worth element. With one of those plans, the insurance firm transfers a section of your regular monthly costs payments right into a cash money worth account. This account gains passion or is invested, assisting it grow and supply a more substantial payout for your beneficiaries.

With a level term life insurance policy policy, this is not the instance as there is no cash money value part. As an outcome, your plan won't grow, and your death benefit will never ever raise, consequently limiting the payment your recipients will get. If you want a plan that gives a fatality advantage and builds money value, look right into entire, global or variable plans.

The 2nd your plan ends, you'll no longer live insurance policy protection. It's commonly possible to restore your plan, however you'll likely see your costs increase substantially. This could offer problems for retired people on a fixed revenue because it's an additional expense they may not be able to afford. Degree term and lowering life insurance offer similar policies, with the primary distinction being the fatality advantage.

It's a type of cover you have for a specific amount of time, called term life insurance policy. If you were to die while you're covered for (the term), your liked ones obtain a fixed payout concurred when you obtain the policy. You simply select the term and the cover quantity which you could base, for instance, on the cost of increasing kids till they leave home and you could make use of the payment in the direction of: Helping to settle your home mortgage, financial debts, charge card or finances Assisting to spend for your funeral costs Helping to pay college charges or wedding celebration prices for your youngsters Aiding to pay living costs, replacing your revenue.

What is Annual Renewable Term Life Insurance? Key Considerations?

The policy has no cash money worth so if your payments quit, so does your cover. If you take out a level term life insurance policy you can: Choose a dealt with quantity of 250,000 over a 25-year term.

{kind=link}

Latest Posts

Burial Insurance No Waiting Period

Cheap Term Life Insurance Instant Quote

Life Debit Funeral Insurance