All Categories

Featured

Table of Contents

Costs are normally lower than whole life plans. With a level term plan, you can pick your protection amount and the policy size.

And you can not squander your plan during its term, so you won't get any monetary gain from your past coverage. As with other kinds of life insurance policy, the expense of a degree term plan depends upon your age, protection requirements, employment, lifestyle and health. Typically, you'll locate a lot more budget-friendly insurance coverage if you're more youthful, healthier and much less high-risk to insure.

Because level term premiums stay the same throughout of insurance coverage, you'll know precisely how much you'll pay each time. That can be a huge aid when budgeting your expenses. Level term insurance coverage likewise has some flexibility, enabling you to customize your policy with added features. These frequently been available in the type of cyclists.

You may have to satisfy details conditions and qualifications for your insurer to pass this biker. Additionally, there might be a waiting duration of up to six months prior to taking impact. There likewise could be an age or time limit on the insurance coverage. You can include a youngster rider to your life insurance coverage plan so it likewise covers your youngsters.

What is included in Affordable Level Term Life Insurance coverage?

The survivor benefit is normally smaller, and insurance coverage normally lasts till your youngster turns 18 or 25. This rider may be an extra affordable way to assist guarantee your children are covered as cyclists can usually cover multiple dependents simultaneously. As soon as your kid ages out of this coverage, it may be possible to convert the biker right into a brand-new plan.

When comparing term versus long-term life insurance policy, it is essential to keep in mind there are a few different kinds. The most usual sort of irreversible life insurance coverage is entire life insurance policy, yet it has some essential differences compared to level term insurance coverage. Here's a basic summary of what to think about when contrasting term vs.

Entire life insurance policy lasts for life, while term coverage lasts for a details period. The costs for term life insurance policy are commonly less than whole life insurance coverage. However, with both, the premiums continue to be the exact same throughout of the policy. Entire life insurance has a cash value part, where a part of the costs might grow tax-deferred for future requirements.

Is there a budget-friendly What Is Level Term Life Insurance? option?

Among the highlights of degree term coverage is that your premiums and your survivor benefit do not transform. With reducing term life insurance policy, your premiums stay the same; nonetheless, the death advantage amount gets smaller sized over time. You may have insurance coverage that begins with a death advantage of $10,000, which could cover a home loan, and then each year, the fatality advantage will certainly lower by a collection quantity or portion.

Due to this, it's typically a much more inexpensive kind of level term insurance coverage. You might have life insurance policy through your employer, yet it may not suffice life insurance for your requirements. The initial step when acquiring a plan is determining just how much life insurance policy you need. Consider factors such as: Age Family size and ages Work condition Revenue Financial obligation Lifestyle Expected last costs A life insurance calculator can assist figure out just how much you require to start.

After choosing on a plan, complete the application. For the underwriting procedure, you may have to supply general personal, wellness, lifestyle and work details. Your insurance firm will identify if you are insurable and the risk you may offer to them, which is reflected in your premium expenses. If you're authorized, sign the documentation and pay your first costs.

You might want to upgrade your recipient details if you've had any type of significant life changes, such as a marital relationship, birth or divorce. Life insurance policy can sometimes feel challenging.

What is a simple explanation of Level Term Life Insurance Calculator?

No, degree term life insurance policy does not have cash value. Some life insurance policy plans have an investment function that enables you to build money worth in time. Term life insurance with fixed premiums. A portion of your premium repayments is alloted and can gain interest gradually, which grows tax-deferred during the life of your insurance coverage

These plans are usually significantly much more costly than term insurance coverage. You can: If you're 65 and your coverage has run out, for example, you might desire to buy a new 10-year level term life insurance policy.

What is the process for getting Affordable Level Term Life Insurance?

You may be able to convert your term protection right into a whole life policy that will certainly last for the rest of your life. Several types of level term policies are exchangeable. That indicates, at the end of your insurance coverage, you can convert some or every one of your plan to entire life coverage.

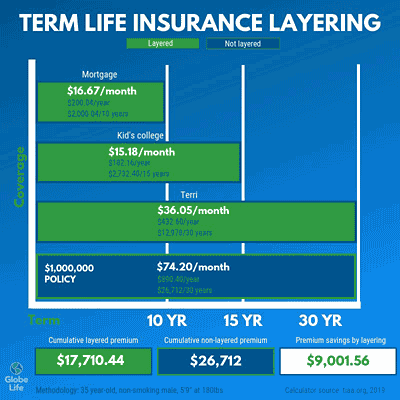

Level term life insurance policy is a policy that lasts a collection term generally in between 10 and thirty years and includes a degree fatality advantage and degree costs that remain the exact same for the whole time the plan is in result. This suggests you'll recognize precisely how much your settlements are and when you'll have to make them, allowing you to spending plan appropriately.

Degree term can be an excellent option if you're aiming to purchase life insurance protection for the very first time. According to LIMRA's 2023 Insurance Barometer Research, 30% of all grownups in the U.S. requirement life insurance coverage and don't have any kind of sort of plan yet. Level term life is foreseeable and budget-friendly, that makes it among the most preferred types of life insurance policy

A 30-year-old male with a similar account can anticipate to pay $29 per month for the very same coverage. AgeGender$250,000 coverage amount$500,000 insurance coverage quantity$1 million coverage amount20Female$15$23$34Male$19$29$4830Female$15$23$37Male$18$29$4940Female$22$35$61Male$25$43$7550Female$44$78$139Male$57$102$18860Female$108$194$355Male$149$268$500 Collapse table Method: Ordinary regular monthly rates are determined for male and women non-smokers in a Preferred health category obtaining a 20-year $250,000, $500,000, or $1,000,000 term life insurance policy policy.

What are the benefits of Level Term Life Insurance Coverage?

Rates might differ by insurance company, term, protection quantity, health and wellness class, and state. Not all policies are offered in all states. It's the least expensive type of life insurance policy for most individuals.

It permits you to spending plan and plan for the future. You can easily factor your life insurance right into your budget plan since the premiums never ever alter. You can intend for the future just as quickly due to the fact that you recognize exactly just how much money your enjoyed ones will certainly get in the occasion of your lack.

Level Term Life Insurance

In these situations, you'll usually have to go with a brand-new application process to get a better price. If you still need insurance coverage by the time your degree term life policy nears the expiration day, you have a few choices.

{kind=link}

Latest Posts

Burial Insurance No Waiting Period

Cheap Term Life Insurance Instant Quote

Life Debit Funeral Insurance